Austin Housing Market Has Not Stabilized: What the Builder Accounting and MLS Numbers Are Actually Hiding

Everyone keeps saying the Austin housing market has stabilized.

Let's look at what is actually happening rather than what the spreadsheets are performing.

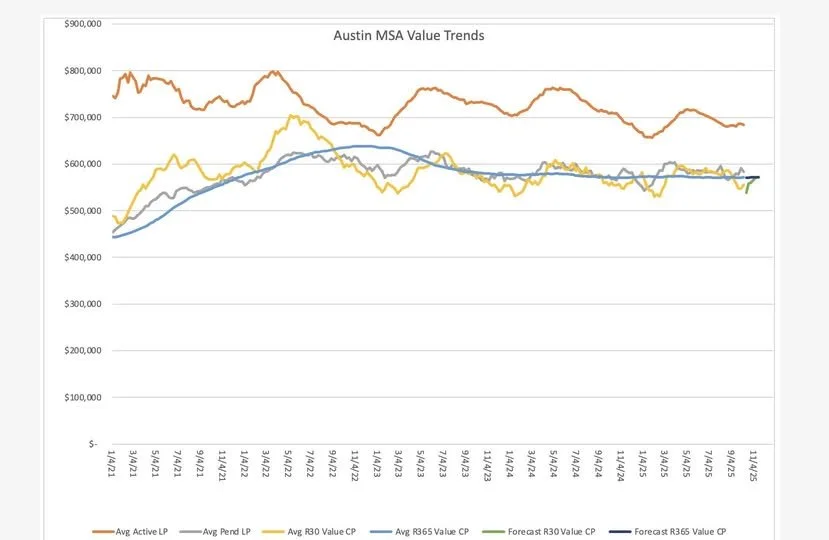

On paper, Austin single-family home values dropped roughly ten percent from the pandemic peak. Six hundred thirty-nine thousand in December of 2022 down to around five hundred seventy thousand by late 2024. The people managing the narrative call that a modest correction. A healthy normalization. Proof that the market found its floor and is ready to recover.

The short-term charts tell a different story. From the peak of seven hundred four thousand, that is a decline closer to twenty-five percent. That is not a correction. That is a faceplant. The difference between those two numbers is not a rounding error. It is the distance between a talking point and a reality, and right now the talking point is winning the media cycle while the reality continues doing what it was already doing.

But here is the part that makes even those numbers too generous.

The builders figured out that the way to protect the optics of market health without actually delivering market health is to disguise price cuts as marketing expenses. Rate buydowns to five and a quarter, five and a half percent when the prevailing market rate sits north of seven. Tens of thousands of dollars in effective price concessions recorded not as price reductions but as advertising costs. The transaction closes at the listed price. The accounting department reflects a healthy market. The MLS data stays clean. And the actual value exchanged in the transaction is something materially different from what any of those systems report.

It is a shell game with institutional polish applied to it.

The buyer believes they got a deal on the rate. The builder maintains the fiction of price stability. The resale market, which cannot offer rate buydowns funded by a corporate balance sheet, sits largely frozen because it cannot compete with incentives it cannot afford to replicate. And the data that everyone is quoting to justify a recovery narrative is measuring the listed price of transactions engineered to obscure the actual price of transactions.

When you factor in the effective value of those invisible incentives, roughly three percent on average, you are looking at another seventeen thousand dollars off that five hundred seventy thousand average. Which puts the real floor not at five hundred seventy but closer to five hundred fifty-three thousand. Which would make this not a stabilization but potentially the lowest point in the entire correction cycle, happening quietly behind a curtain of creative accounting while the headlines call it a bottom.

So when someone tells you Austin has bottomed, the question worth asking is bottomed based on what exactly. The MLS numbers that reflect listed prices rather than effective transaction values. The builder's accounting department that classifies price cuts as marketing expenses. Or the actual prices people are paying once you strip the smoke and mirrors out of the data and look at what the market is genuinely clearing at.

This recovery is not being driven by affordability. It is being driven by financial engineering. Builders are not selling confidence in the market. They are buying time with their balance sheets, burning cash to maintain the illusion of stability long enough to move inventory before the curtain gets pulled back.

That game has a duration. Balance sheets that fund rate buydowns and incentive packages to keep transaction prices artificially elevated eventually reach the point where the math stops working. When that happens, the data will finally catch up to the reality that has been building quietly behind the reported numbers. Austin has not stabilized. It is still correcting, just slowly enough and obscured enough that the headlines have not noticed yet.

The sophisticated capital in this market already knows this. The question is not whether the adjustment continues. It is when the accounting gets too heavy to carry and the real floor becomes the reported floor.

Position accordingly.

If you want to talk through what the Austin market actually looks like beneath the reported numbers and how to evaluate deals in an environment where the data requires translation, let's talk. Schedule a call at calendly.com/jeph-reit