What Flat Rent Growth Actually Means for Multifamily Investors

The rent graph is flat. That's not the whole story.

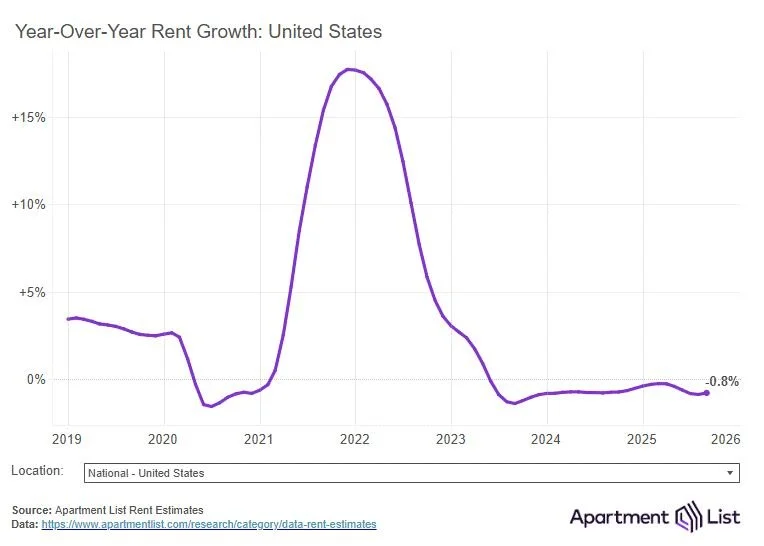

Apartment List has the numbers. National rents have hovered around zero percent growth for the better part of two years. You can pull up the chart, look at the line, and conclude that the multifamily market is cooling. A lot of people are doing exactly that. Most of them are missing the point.

A graph shows you the outcome. It does not explain the mechanics. And in real estate, the mechanics are where the money is made or lost.

So why is the line flat? Affordability ran out of runway. Renters hit their ceiling, and operators found out the hard way that you cannot push rents past what people can actually pay. Certain Sunbelt metros flooded the market with supply, thousands of new units hitting the street at the same time, which dragged asking rents down and kept them there. On top of that, household formation slowed. People doubled up, moved back home, or simply stopped forming new households at the pace that was being projected. And some operators, riding the wave of automatic annual bumps, kept raising rents past the point of reason until vacancy told them to stop.

Those are the levers that moved the line. The line itself tells you nothing useful.

Here's what else the chart is hiding: national averages are not a market. They're a weighted blend of dozens of markets behaving very differently from one another. The Sunbelt oversupply story is real, and it is dragging the national number down. But not every market looks like Phoenix or Austin right now. Some markets are tighter. Some submarkets within oversupplied metros are performing better than the headline suggests. The average flattens all of that out and hands you a number that is technically accurate and practically useless.

The investors who got hurt over the last two years are the ones who treated rent growth as automatic. They bought deals underwritten on the assumption that rents would keep climbing, took on the debt to match, and then watched the market stop cooperating. That is not bad luck. That is bad underwriting dressed up as a business plan.

The operators who are outperforming right now are doing the work that was always supposed to be done. They are focused on retention, because a vacant unit loses money from the day the tenant leaves until the day a new lease starts. They are focused on renewals, because acquiring a new tenant costs more than keeping one. They are managing expenses with discipline, because when you cannot grow your top line you had better protect your margins. They are creating actual value, improving the product, improving the experience, rather than waiting for the market to do the heavy lifting.

None of this is new. It just looks new to people who got used to the easy version.

If you understand what is actually driving the numbers, you can identify which levers still move. Occupancy, renewals, expense control, operational efficiency, these are not consolation prizes. They are the fundamentals. The chart will catch up eventually. The operators who stay focused on the fundamentals will be in a much stronger position when it does.

Thirty years in this business has taught me that the people who panic at a flat line and the people who ignore a flat line tend to end up in similar places. Neither one asked why.

If you want to talk through what the numbers in your market are actually telling you, and what moves still make sense, let's get on a call.

You can schedule time directly at calendly.com/jeph-reit.